Credit scores are a curious thing. On the one hand, they say a great deal about us; they indicate, at least to a certain extent, our fiscal responsibility. They’re used by banks, credit card companies, car dealerships, and many other institutions to determine our “creditworthiness.”

Credit scores are a curious thing. On the one hand, they say a great deal about us; they indicate, at least to a certain extent, our fiscal responsibility. They’re used by banks, credit card companies, car dealerships, and many other institutions to determine our “creditworthiness.”

What’s strange, then, is how difficult it can be to know just what your credit score is – and how to find it. I’ll give you some suggestions in a moment for how you can get your credit score for free.

For right now, though, let’s put things in perspective. You can win the credit score game!

I want to pull back the curtain just a little bit on the world of credit scores and show you how the rest of the country stacks up and how your credit score compare – even if you don’t know what your own credit score is right at this moment.

[For the full infographic, click here]

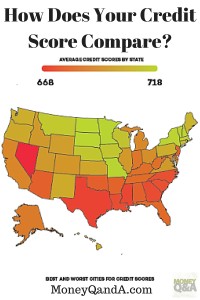

How does your score stack up?

The map above provides a bird’s eye view of America, along with its credit score range.

What’s immediately striking is just how small that range really is. The lowest credit scores hover around 668, while the highest scores are around 718. That’s a range of only 50 points.

In other words, 50 points is all that separates America’s best credit scores from its worst.

Also of note is the rather subtle shift from the lower credit scores of the south to the higher scores farther north. In fact, the Midwest is home to some of the best credit scores in the country. The shades of green and red you see on the map are only averages, but it still paints a fairly clear picture of our country’s socioeconomic climate – even if may not be precisely what we expected.

What goes into a credit score?

Knowing your credit score is definitely important, but it’s even more important to know what that number means.

The most common credit measurement system is known as the myFICO score. It’s a proprietary system, which means the Fair Isaac Corporation – the company that created the metric – has, historically, been rather tight-lipped about the criteria they use to measure it. 90% of top lenders use FICO® Scores

Nevertheless, we now know the general categories used by Fair Isaac to arrive at that all-important number:

- Payment history (35%)

- Amount owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Type of credit used (10%)

The good news is that there is no single piece of data that influences your credit score; it relies on a number of factors.

Nevertheless, those factors are pretty specific, which means that certain demographics – the underemployed college grad, for example – are particularly susceptible to poor credit scores.

All of this simply drives home the fact that getting an early start on building your credit history – even if it’s a solitary, seldom-used credit card – is absolutely essential.

Finding your score

As secretive as myFICO and its inner workings may be, you still have a number of options for monitoring your credit score – and you can most likely do it for free.

Companies like CreditSesame.com, Credit Karma, and Mint.com all offer free credit monitoring services at the modest cost of some of your personal information. These services have been well received by users and have excellent track records when it comes to privacy.

However, if you’d prefer to consolidate the number of corporate entities that have access to your most personal data – and given our current state of very justified paranoia, you’re probably right to do so – you should know that your financial institution or credit card company may also offer credit scores and report. It’s worth taking a look.

If anything has become clear, though, it’s that the difference between good credit and bad credit is a much shorter journey than you may have expected.

So find your state on that map. How does your score stack up? If your answer is I don’t know, it’s probably time to make a change.

About the Author:

Daniel Faris studied creative writing and journalism at Susquehanna University before graduating in 2011. He now owns and operates a small tech blog, The Byte Beat. You can also find his alter ego discussing progressive music over at New Music Friday.

So hard to stay on top of your credit score.

Heard the best tip ever recently from an interview I did. Most know that you can argue errors on your report by contacting the company that put the item on your report. If they don’t reply in 30 days then you can contact the credit bureau and have it removed…but

it also works for anything on your report. Miss a payment on your Macy’s card a few years ago? Write them a letter contesting the missed payment. If the card has been closed, they’re probably not going to take the time to reply. Boom. You can get it taken off your report.

I keep checking my credit as many times as possible every year, just to make sure that I keep track of me credit card history.

It’s another learning method on How Does Your Credit Score Compare to the Rest of the US. This is very helpful and useful. I learned and many great tips here. Thanks for sharing the article. Great post!

“What’s immediately striking is just how small that range really is. The lowest credit scores hover around 668, while the highest scores are around 718. That’s a range of only 50 points.

In other words, 50 points is all that separates America’s best credit scores from its worst.”

That’s the range of the state averages. There is a MUCH wider range in individual scores. A score of 668 is nowhere near the worst score, and scores max out in the 800’s.